In today’s interconnected business landscape, organizations face increasing scrutiny and demands for transparency regarding their control environment and data security practices. To address these concerns, various types of System and Organization Controls (SOC) reports have emerged as essential tools for assessing and communicating a company’s control effectiveness. Among these reports, SOC 1, SOC 2, and SOC 3 are widely recognized. In this article, we will delve into theSOC 1 vs SOC 2 vs SOC 3, exploring their purposes, scopes, and examination processes, while providing insights into their respective use cases.

Introduction

SOC reports are a standardized framework developed by the American Institute of Certified Public Accountants (AICPA) to evaluate and report on the controls implemented by organizations. Each SOC report serves a specific purpose and targets different stakeholders. Furthermore, understanding the distinctions between SOC 1, SOC 2, and SOC 3 is crucial for organizations seeking to assure their clients and partners regarding their control environment and data security.

SOC 1

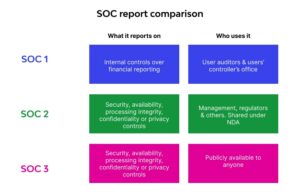

SOC 1 reports are designed to assess the internal controls over financial reporting. They are often relevant for service organizations whose services impact the financial statements of their clients. SOC 1 reports assure user entities that their financial information is accurate and reliable.

SOC 1 reports evaluate the effectiveness of control activities relevant to financial reporting, including processes for risk assessment, monitoring, and operational activities. These controls are typically assured for Attestation Engagements (SSAE) No. 18, which replaced the previous SAS 70 standard.

During a SOC 1 examination, an independent auditor assesses the design and operational effectiveness of the controls defined by the service organization. The auditor provides an opinion on whether they operating effectively over assure specified period.

SOC 2

SOC 2 reports focus on the controls related to security, availability, processing integrity, confidentiality, and privacy (referred to as the Trust Services Criteria). Furthermore, they provide valuable insights into an organization’s non-financial controls, which are essential for ensuring the security and privacy of sensitive information.

SOC 2 reports are based on the Trust Services Criteria (TSC), which define the principles and criteria for evaluating an organization’s controls. The TSC encompasses five key areas: security, availability, processing integrity, confidentiality, and privacy. Furthermore, organizations can choose to be assessed on one or more of these areas based on their specific requirements.

During a SOC 2 examination, an independent auditor evaluates the controls implemented by the service organization based on the selected Trust Services Criteria. The examination includes an assessment of the design and operational effectiveness of these controls. The auditor issues a report that describes the controls tested, the results of the examination, and any identified control deficiencies or areas for improvement.

SOC 3

SOC 3 reports are designed for organizations that want to provide a high-level overview of their control environment to a broad audience, including potential customers and business partners. Furthermore, these reports are intended for public consumption and are often used to demonstrate a commitment to security and data privacy.

Similar to SOC 2, SOC 3 reports are based on the Trust Services Criteria. However, SOC 3 reports provide a summarized version of the examination findings and do not include detailed descriptions of controls and test results.

The examination process for SOC 3 is similar to SOC 2, where an independent auditor assesses the controls based on the selected Trust Services Criteria. However, the resulting report is a general-use report that can be freely distributed to the public.

SOC 1 vs SOC 2 vs SOC 3

While SOC 1, SOC 2, and SOC 3 share similarities in terms of the examination process and reliance on controls, there are key differences that organizations should consider:

- Purpose: SOC 1 focuses on financial reporting controls, SOC 2 assesses non-financial controls based on the Trust Services Criteria, and SOC 3 provides a summarized overview of controls for public consumption.

- Target Audience: SOC 1 reports are intended for user entities and their auditors, SOC 2 reports cater to a narrower audience seeking detailed insights into non-financial controls, and SOC 3 reports target a broader audience, including potential customers and business partners.

- Distribution: SOC 1 and SOC 2 reports are restricted to specific parties involved in the service organization’s business relationships, while SOC 3 reports can be freely distributed to the public.

- Level of Detail: SOC 1 and SOC 2 reports provide detailed descriptions of controls and test results, whereas SOC 3 reports offer a more condensed summary of the examination findings.

Organizations should carefully evaluate their specific needs and the expectations of their stakeholders when determining which type of SOC report is most suitable for their business.

Conclusion

In a world where trust and data security are paramount, SOC reports serve as vital tools for organizations to communicate their control environment and provide assurance to their stakeholders. SOC 1, SOC 2, and SOC 3 reports target different aspects of controls and cater to specific audiences. Understanding the purposes, scopes, and examination processes of these reports is essential for organizations to make informed decisions and meet the expectations of their clients, partners, and regulators.

If you are looking to implement any of the Infosec compliance frameworks such as SOC 2 compliance, HIPAA, ISO 27001, and GDPR compliance, Impanix can help. Book a Free consultation call with our experts or email us at [email protected] for inquiries.